The Pradhan Mantri Mudra Yojana, commonly known as PMMY or Mudra Loan, is a Government of India credit scheme designed to help micro and small business owners access formal business finance.

Under the scheme, eligible entrepreneurs can approach participating banks, Non-Banking Financial Companies and Microfinance Institutions for collateral-free loans to start or expand income-generating businesses.

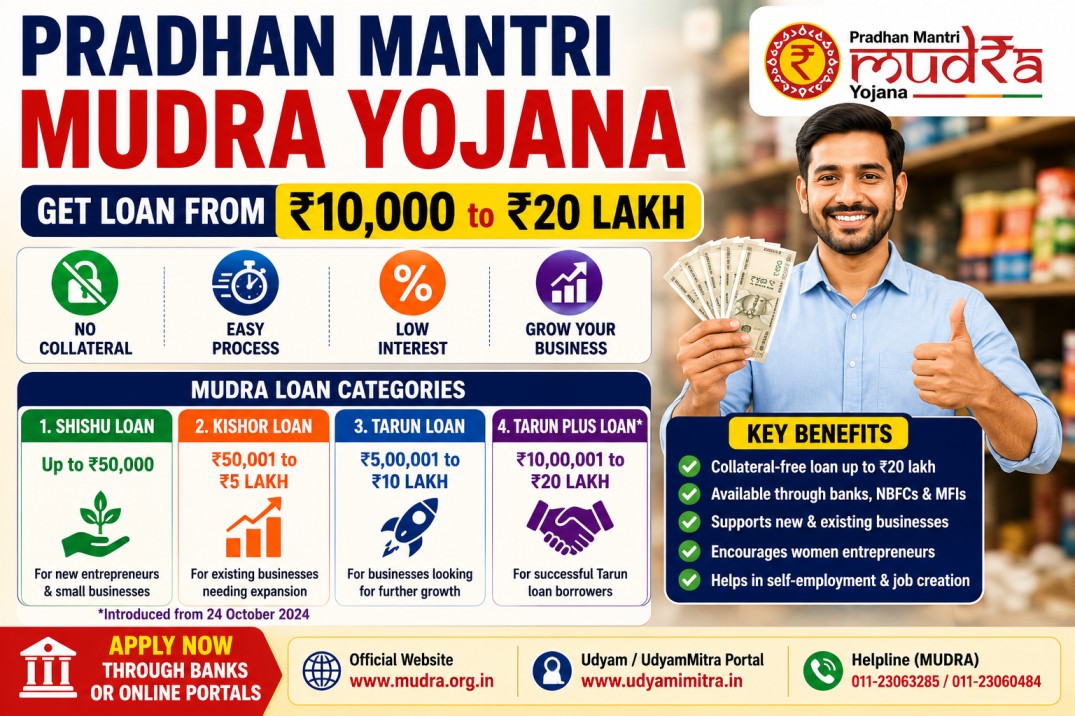

Mudra loans are available under four categories:

- Shishu

- Kishor

- Tarun

- Tarun Plus

The regular categories provide loans up to ₹10 lakh. Under the newer Tarun Plus category, eligible borrowers who previously received and successfully repaid a Tarun loan may obtain credit above ₹10 lakh and up to ₹20 lakh.

Important: Nuvelloza.com is an independent informational website. We are not affiliated with MUDRA, the Ministry of Finance, any bank or any government authority. Loan approval, interest rates, repayment terms and required documents are decided by the participating lender.

Pradhan Mantri Mudra Yojana 2026 Overview

| Particular | Details |

|---|---|

| Scheme name | Pradhan Mantri Mudra Yojana |

| Short name | PMMY |

| Launch date | April 8, 2015 |

| Main purpose | Business finance for eligible micro enterprises |

| Maximum standard Mudra loan | Up to ₹10 lakh |

| Maximum Tarun Plus loan | Up to ₹20 lakh |

| Security | Collateral-free under applicable PMMY rules |

| Eligible sectors | Manufacturing, trading, services and eligible allied agricultural activities |

| Lending institutions | Banks, NBFCs and Microfinance Institutions |

| Interest rate | Decided by the lender |

| Approval | Subject to lender appraisal and eligibility |

What Is Pradhan Mantri Mudra Yojana?

Pradhan Mantri Mudra Yojana was launched on April 8, 2015 to improve access to institutional, collateral-free credit for micro enterprises.

The scheme supports income-generating small-business activities in manufacturing, trading and services. Eligible activities allied to agriculture, such as poultry, dairy and similar enterprises, may also be financed.

MUDRA does not generally provide the loan directly to an individual borrower. Loans are sanctioned and disbursed by participating financial institutions.

These may include:

- Scheduled commercial banks

- Public-sector banks

- Private banks

- Regional Rural Banks

- Small Finance Banks

- Cooperative banks

- Non-Banking Financial Companies

- Microfinance Institutions

Why Was Mudra Yojana Started?

Many small shopkeepers, artisans, service providers, street businesses and self-employed workers find it difficult to obtain formal business finance.

They may lack:

- Property to offer as security

- A long business-credit history

- Audited financial statements

- Access to established banking relationships

- Sufficient funds to buy equipment or inventory

PMMY was created to help qualifying micro enterprises access formal credit without depending entirely on expensive informal borrowing.

Mudra Loan Categories

1. Shishu Loan

Loan amount: Up to ₹50,000

The Shishu category is generally intended for very small or early-stage businesses.

It may be suitable for:

- Small street businesses

- Home-based enterprises

- Tailoring work

- Repair services

- Food stalls

- Small kiosks

- Artisans

- First-time micro entrepreneurs

2. Kishor Loan

Loan amount: Above ₹50,000 and up to ₹5 lakh

The Kishor category may suit businesses that have already started operating and need additional funds for development or expansion.

The money may be used for:

- Purchasing machinery

- Increasing stock

- Improving a shop

- Buying tools

- Meeting working-capital needs

- Expanding services

3. Tarun Loan

Loan amount: Above ₹5 lakh and up to ₹10 lakh

The Tarun category is intended for more established micro enterprises requiring a larger amount for business growth.

Applicants may need to provide stronger evidence of:

- Business activity

- Income or turnover

- Repayment capacity

- Bank transactions

- Proposed use of funds

4. Tarun Plus Loan

Loan amount: Above ₹10 lakh and up to ₹20 lakh

Tarun Plus was introduced with effect from October 24, 2024.

This category is specifically intended for entrepreneurs who:

- Previously received a Mudra loan under the Tarun category; and

- Successfully repaid that Tarun loan

Therefore, a first-time applicant cannot normally apply directly for ₹20 lakh under Tarun Plus merely by submitting a new business plan.

Mudra Loan Categories at a Glance

| Category | Loan amount | Typical business stage |

|---|---|---|

| Shishu | Up to ₹50,000 | Starting or very small business |

| Kishor | Above ₹50,000 to ₹5 lakh | Developing business |

| Tarun | Above ₹5 lakh to ₹10 lakh | Established or expanding micro enterprise |

| Tarun Plus | Above ₹10 lakh to ₹20 lakh | Successful previous Tarun borrowers |

Who Can Apply for a Mudra Loan?

An individual with an eligible business plan for a micro enterprise may apply through a participating lender.

Potential applicants may include:

- Shopkeepers

- Artisans

- Self-employed workers

- Service providers

- Small manufacturers

- Traders

- Food-business operators

- Tailors

- Beauty-salon owners

- Repair-shop owners

- Transport operators

- Small contractors

- Women entrepreneurs

- New micro-business owners

- Existing micro-enterprise owners

The business should generally involve an income-generating activity in:

- Manufacturing

- Trading

- Services

- Eligible activities allied to agriculture

Official PMMY information states that eligible individuals with small-business plans may apply for income-generating activities in these sectors.

General Eligibility Conditions

Although each lender applies its own credit policy, applicants are generally expected to:

- Be eligible to borrow under the lender’s rules

- Have a genuine business or business proposal

- Use the funds for an eligible income-generating activity

- Provide acceptable identity and address documents

- Demonstrate the ability to repay the loan

- Not be a wilful defaulter

- Provide accurate business and financial information

- Meet the lender’s age and credit requirements

There is no universal official rule guaranteeing approval to every Indian citizen aged between 18 and 70. Age limits and applicant requirements may vary by lender.

Can Farmers Apply for a Mudra Loan?

Mudra loans are not intended for ordinary crop cultivation expenses.

However, eligible income-generating activities allied to agriculture may be considered, including certain businesses connected with:

- Dairy

- Poultry

- Fisheries

- Beekeeping

- Food processing

- Agricultural-services businesses

- Transport of agricultural produce

The exact activity must be acceptable to the participating lender under current PMMY rules.

What Can a Mudra Loan Be Used For?

An approved Mudra loan may be used for legitimate business purposes such as:

- Starting a small business

- Buying machinery

- Purchasing tools or equipment

- Buying business inventory

- Purchasing raw materials

- Renovating business premises

- Expanding an existing shop

- Purchasing an eligible commercial vehicle

- Funding working-capital requirements

- Setting up a service business

- Improving production capacity

- Purchasing computers or business technology

The loan should not be used for unrelated personal expenses.

Applicants should clearly explain how the loan will generate business income and how it will be repaid.

Examples of Businesses That May Qualify

Eligible activities may include:

- Tailoring shops

- Beauty salons

- Mobile-repair shops

- Grocery stores

- Food stalls

- Bakeries

- Small restaurants

- Manufacturing units

- Handicraft businesses

- Printing services

- Computer-service centres

- Auto-rickshaw or eligible transport services

- Electrical-repair businesses

- Carpenter workshops

- Plumbing services

- Small trading businesses

- Dairy-related enterprises

- Poultry-related enterprises

Eligibility depends on the nature of the business and the participating lender’s appraisal.

Main Benefits of Mudra Yojana

Collateral-Free Business Credit

The main feature of PMMY is access to collateral-free institutional credit for eligible micro enterprises.

Tarun Plus loans up to ₹20 lakh are also covered under the expanded guarantee framework for eligible previous Tarun borrowers.

Collateral-free does not mean the borrower has no repayment responsibility. The applicant remains legally responsible for repaying the loan.

Support for New and Existing Businesses

PMMY may support:

- New businesses

- Existing micro enterprises

- Self-employment activities

- Business expansion

- Equipment purchases

- Working-capital requirements

Multiple Lending Options

Applicants may approach several categories of participating financial institutions instead of relying on one type of bank.

Support for Women Entrepreneurs

Women entrepreneurs form a major group of Mudra borrowers. Government data has shown that a substantial proportion of PMMY loans have been provided to women.

This does not mean that every woman applicant is automatically approved. The lender must still assess the application.

Formal Business Finance

A Mudra loan can help small businesses enter the formal banking system, build repayment history and reduce dependence on informal moneylenders.

Is a Mudra Loan Interest-Free?

No.

PMMY is a loan programme, not an interest-free grant.

Interest is charged by the participating lender according to factors such as:

- Loan amount

- Business activity

- Applicant’s credit profile

- Repayment capacity

- Loan tenure

- Internal lender policy

- Applicable benchmark rates

There is no single fixed Mudra interest rate that applies to all banks and borrowers.

Avoid publishing a guaranteed interest range such as 9% to 12%, because the actual rate may be lower or higher depending on the lender and applicant.

Mudra Loan Repayment Period

The repayment period is determined by the lender after considering:

- Loan purpose

- Cash flow

- Loan amount

- Business income

- Type of asset financed

- Moratorium, where applicable

- Borrower’s repayment capacity

Depending on the loan structure, repayment may occur through:

- Monthly instalments

- Term-loan instalments

- Working-capital arrangements

- Mudra Card usage

- Another lender-approved schedule

Applicants should ask for the total repayment amount, interest rate, processing charges and instalment schedule before signing.

Documents Required for a Mudra Loan

Documents may vary according to the lender, loan category and business.

Commonly requested documents may include:

- Aadhaar Card

- PAN Card

- Voter ID or another identity document

- Address proof

- Passport-size photographs

- Bank-account statements

- Existing business-registration proof

- Udyam Registration, where applicable

- GST details, where applicable

- Shop or establishment licence

- Business-plan or project report

- Machinery or equipment quotations

- Supplier quotations

- Income-tax returns, where applicable

- Sales records

- Financial statements

- Proof of business premises

- Partnership documents, where applicable

- Existing loan details

JanSamarth states that online applicants may need documents such as Aadhaar, voter identification, PAN and bank statements, although final requirements depend on the scheme and lender.

How to Prepare a Simple Business Plan

A useful business plan should explain:

- What the business does

- Whether it is new or existing

- Where the business will operate

- Who the customers are

- How much money is required

- How the loan will be used

- Expected monthly sales

- Expected monthly expenses

- Estimated monthly profit

- Proposed repayment source

- Applicant’s experience

- Existing investment in the business

Do not exaggerate expected profits. Banks may compare your estimates with actual market conditions and account activity.

How to Apply for a Mudra Loan Online

Online availability may depend on the lender and scheme portal.

Step 1: Check Your Loan Category

Determine whether your requirement falls under:

- Shishu

- Kishor

- Tarun

- Tarun Plus

Remember that Tarun Plus is restricted to eligible borrowers who successfully repaid a previous Tarun loan.

Step 2: Visit an Official Platform

Applicants may check PMMY eligibility and participating lenders through the Government’s JanSamarth platform or approach a participating bank directly.

Udyam Registration is a business-registration platform. Registering on Udyam does not itself guarantee a Mudra loan.

Step 3: Register and Verify Your Identity

Provide the requested information, such as:

- Name

- Mobile number

- Aadhaar

- PAN

- Address

- Business details

Complete OTP or identity verification.

Step 4: Enter Business Information

Describe:

- Type of business

- Business location

- Loan amount needed

- Purpose of the loan

- Existing turnover

- Expected income

- Employment generated

- Current bank details

Step 5: Upload Documents

Upload clear and valid copies of all requested documents.

Documents that are unreadable, inconsistent or expired may delay the application.

Step 6: Select a Lender

Where the portal allows, review available participating lenders and select an appropriate option.

The final interest rate and approval terms come from the lender, not from the online portal alone.

Step 7: Submit the Application

Review all details carefully before submitting.

Save the application or reference number for tracking.

Step 8: Complete Bank Verification

The lender may contact you for:

- Additional documents

- Business verification

- Credit checks

- Interview or discussion

- Site inspection

- Revised project estimates

- Bank-account verification

Submitting the online form does not guarantee approval.

How to Apply Offline

Applicants may also visit a nearby participating financial institution.

Offline Application Steps

- Visit a participating bank, NBFC or Microfinance Institution.

- Ask for the PMMY or Mudra loan application form.

- Select the appropriate category.

- Fill in personal and business details.

- Attach the required documents.

- Submit the business plan and quotations.

- Obtain an acknowledgement.

- Cooperate with the lender’s verification process.

- Review the sanction letter before accepting the loan.

MUDRA provides common application forms and banker resources for eligible categories.

Does MUDRA Approve the Loan Directly?

Generally, no.

MUDRA supports and refinances lending institutions, while the participating bank, NBFC or Microfinance Institution evaluates the borrower and sanctions the loan.

The lender decides:

- Whether the applicant qualifies

- Approved loan amount

- Interest rate

- Repayment tenure

- Documentation

- Business verification

- Disbursement conditions

Is Collateral Required?

PMMY is structured as collateral-free credit for eligible micro enterprises under its guarantee arrangements.

However, lenders may still require:

- Hypothecation of assets purchased with the loan

- Business documents

- Personal guarantees where legally and operationally permitted

- Repayment undertakings

- Insurance for financed assets

- Other documentation

Applicants should ask the lender to explain all security and documentation requirements in writing.

What Is a Mudra Card?

A Mudra Card may be issued for eligible working-capital loans.

It can allow the borrower to access sanctioned working capital according to the lender’s rules.

It should be used only for approved business expenses and must be repaid under the applicable loan terms.

Not every Mudra borrower automatically receives the same card facility.

Common Reasons for Mudra Loan Rejection

A loan application may be rejected or approved for a smaller amount because of:

- Poor credit history

- Previous loan default

- Weak repayment capacity

- Incomplete business plan

- Unrealistic income estimates

- Missing documents

- Mismatched Aadhaar or PAN details

- Unclear purpose of funds

- Business activity not eligible

- Excessive existing debt

- Insufficient bank transactions

- Applicant cannot prove business experience

- False or misleading information

- Tarun Plus applicant has not repaid a previous Tarun loan

A rejected applicant may ask the lender for the reason and correct genuine deficiencies before applying again.

Mudra Loan vs Regular Business Loan

| Feature | Mudra Loan | Regular business loan |

|---|---|---|

| Main audience | Micro enterprises | Businesses of different sizes |

| Maximum under scheme | Up to ₹20 lakh for eligible Tarun Plus borrowers | Depends on lender |

| Collateral | Collateral-free under PMMY conditions | May be secured or unsecured |

| Interest rate | Decided by lender | Decided by lender |

| Government subsidy | Not automatically provided | Usually not applicable |

| Approval guaranteed | No | No |

| Credit assessment | Required | Required |

Do not describe Mudra loans as automatically cheaper than every regular business loan. The actual cost depends on the lender and applicant.

Fraud and Safety Tips

- Do not pay an agent for guaranteed approval.

- MUDRA says it has not appointed agents or middlemen for obtaining Mudra loans.

- Apply through official portals or recognised lenders.

- Never share an Aadhaar OTP or bank password.

- Do not send advance approval fees to a personal account.

- Verify the lender’s name and branch.

- Read the sanction letter before signing.

- Check the interest rate and total repayment.

- Keep copies of receipts and submitted documents.

- Do not submit false business information.

Official Mudra Resources

Applicants should use official sources for current information:

- MUDRA official website

- Department of Financial Services

- JanSamarth Government portal

- Participating banks and financial institutions

MUDRA states that loans may be obtained through nearby branches of banks, NBFCs and Microfinance Institutions, with online filing options also available.

Frequently Asked Questions

What is the minimum Mudra loan amount?

There is no universal guaranteed minimum. The sanctioned amount depends on the business need and lender’s assessment. The Shishu category covers loans up to ₹50,000.

What is the maximum Mudra loan amount in 2026?

The maximum is up to ₹20 lakh under Tarun Plus for eligible borrowers who previously took and successfully repaid a Tarun loan.

Other eligible borrowers may apply under Shishu, Kishor or Tarun, with the regular Tarun category extending up to ₹10 lakh.

Can a first-time applicant get ₹20 lakh?

Generally, no. Tarun Plus is intended for successful previous Tarun borrowers.

Is a Mudra loan free money?

No. It is a repayable business loan with interest.

Is there any government subsidy?

PMMY itself is primarily a credit scheme. A borrower should not assume that part of the loan will automatically be waived or subsidised.

Some businesses may qualify separately under another government programme, but that must be verified independently.

Can I apply without collateral?

PMMY provides collateral-free credit under applicable scheme conditions, but the lender still evaluates repayment capacity and may secure the financed business assets.

Can unemployed people apply?

A person planning a genuine eligible business may apply, but the lender will evaluate the project, documents, experience and repayment feasibility.

Is Udyam Registration compulsory?

Requirements may vary depending on the lender and applicant. Some lenders may request Udyam Registration or other business proof.

Udyam registration alone does not guarantee approval.

How long does Mudra approval take?

There is no universal approval period. Processing time depends on the lender, loan category, documents, business verification and credit assessment.

Can I use the loan for personal expenses?

No. Mudra funds should be used for the approved income-generating business purpose.

Final Words

Pradhan Mantri Mudra Yojana can help eligible micro entrepreneurs access formal business finance without traditional collateral.

Before applying:

- Choose the correct loan category

- Prepare a realistic business plan

- Collect complete documents

- Check your credit history

- Apply through an official portal or participating lender

- Understand the interest rate and repayment terms

- Avoid agents promising guaranteed approval

- Remember that Tarun Plus is only for successful previous Tarun borrowers

A Mudra application does not guarantee approval or the full requested amount. The lender makes the final credit decision after evaluating the business and the applicant’s repayment capacity.

Disclaimer

This article is provided only for general informational purposes.

Nuvelloza.com does not provide Mudra loans, process applications, collect loan fees, arrange approvals or represent MUDRA, the Ministry of Finance, JanSamarth or any participating financial institution.

Loan categories, eligibility requirements, interest rates, documents, repayment terms and online facilities may change.

Applicants should verify current information directly through official government sources and the participating lender before submitting an application.